Understanding Title Insurance and Escrow: A Homebuyer's Guide to Smooth Closings in Las Vegas

- platinumtitleandescrow

- 19 ene

- 3 Min. de lectura

Buying a home in Las Vegas is exciting—whether you're eyeing a condo near the Strip, a family home in Summerlin, or an investment property in Henderson. But behind the excitement lies a critical process: title insurance and escrow. These elements protect your investment and ensure the transfer of ownership happens securely and legally.

At Platinum Title and Escrow, we believe informed clients make the best decisions. This educational post breaks down what title insurance and escrow really mean, why they're essential in Nevada's real estate market, and how the process works step by step.

What Is Escrow and Why Does Nevada Use It?

Escrow is a neutral third-party arrangement where a licensed escrow company (like us) acts as an impartial intermediary. We hold funds, documents, and earnest money deposits until all conditions of the purchase agreement are met.

In Nevada—an escrow state—this process is standard for most real estate transactions. It protects everyone involved:

Buyers know their money won't go to the seller until they get clear title.

Sellers know funds are secure and will be disbursed only after they fulfill their obligations.

Lenders ensure their loan is properly secured.

The escrow officer coordinates with your real estate agent, lender, title company, and other parties to keep everything on track.

Step-by-Step: The Escrow and Closing Process in Nevada

Offer Accepted and Escrow Opened Once your offer is accepted, the purchase agreement is sent to the escrow company. You deposit earnest money (typically 1-3% of the purchase price) into escrow as a show of good faith.

Title Search and Preliminary Report We conduct a thorough search of public records to trace the property's ownership history. This reveals any liens, encumbrances, easements, or issues (like unpaid taxes or judgments). A preliminary title report is issued, listing any "clouds" on title that need resolution before closing.

Addressing Title Issues Common problems include old liens, unpaid HOA fees, or recording errors. We work proactively to clear these—often requiring payoffs or releases—so you receive clean title.

Loan Processing and Contingencies Your lender orders an appraisal and underwrites the loan. You complete inspections, appraisals, and any contingencies (e.g., home inspection or financing). We coordinate document requests and updates.

Closing Disclosure and Final Preparations You receive a Closing Disclosure at least three days before closing (required by federal law). This details all costs, fees, and prorations (e.g., property taxes, HOA dues). Review it carefully—we're happy to explain every line.

Signing and Funding In Nevada, buyers and sellers often sign documents separately (not always at the same table). You bring certified funds (cashier's check or wire) for your down payment and closing costs. The lender wires loan proceeds to escrow.

Recording and Disbursement Once everything checks out, we record the deed with the Clark County Recorder's Office. Funds are disbursed: seller gets proceeds, liens are paid off, commissions are distributed, etc. You get the keys, and ownership transfers!

Timelines vary—typically 30-45 days—but cash deals can close faster.

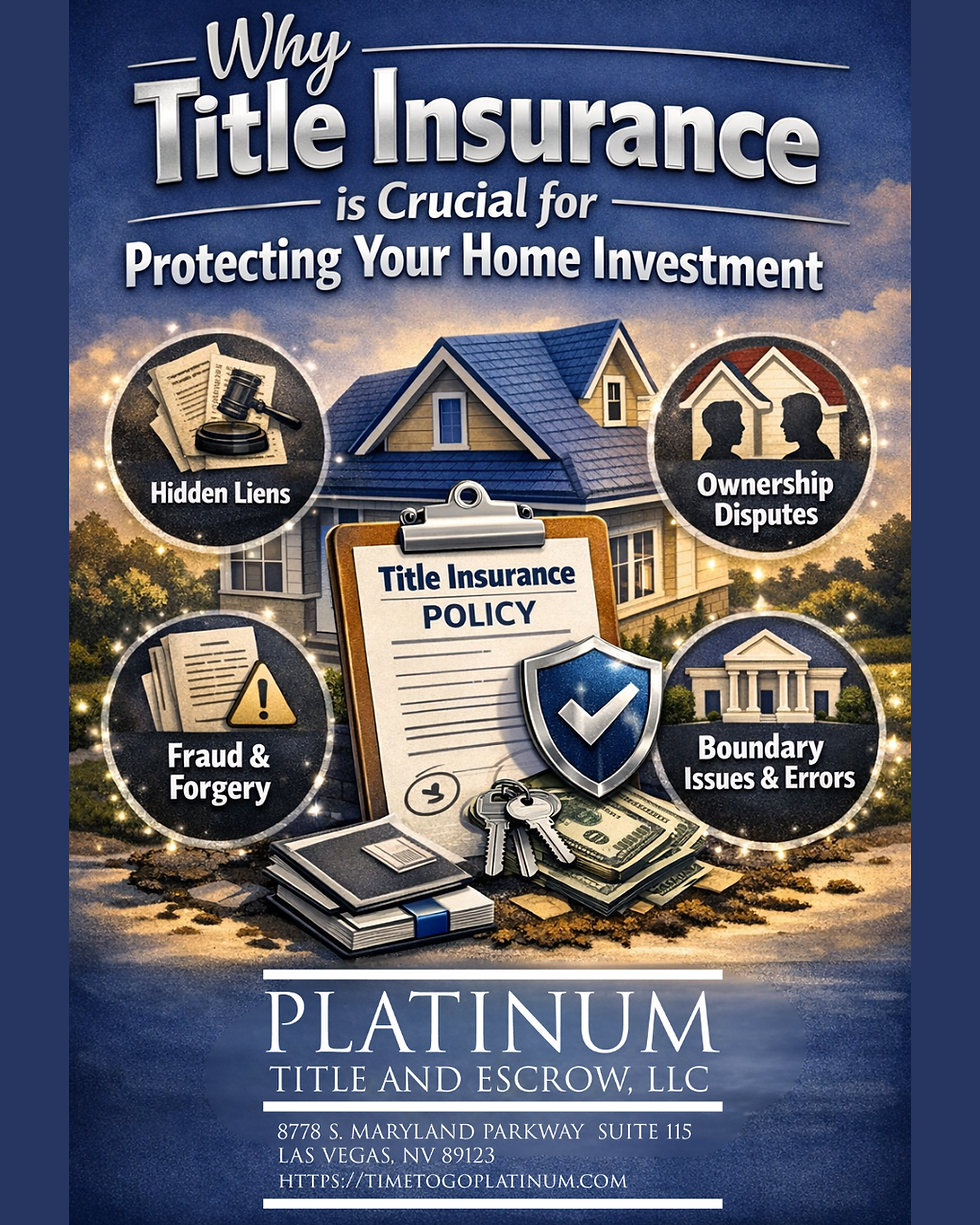

What Is Title Insurance and Why Is It Important?

Title insurance protects against losses from defects in the property's title that existed before you bought it. Unlike homeowners insurance (which covers future events like fire), title insurance covers past issues that might surface later.

Common hidden risks include:

Forged deeds or signatures

Undisclosed heirs claiming ownership

Unrecorded liens or judgments

Errors in public records

Fraud or impersonation

There are two main policies:

Owner's Policy — Protects you (the buyer) for as long as you or your heirs own the property. It's a one-time premium, highly recommended even if not required.

Lender's Policy — Required by your mortgage lender; protects only their interest until the loan is paid off.

In Nevada (including Las Vegas/Clark County), it's customary for the seller to pay for the owner's policy, while the buyer pays for the lender's policy—but this is negotiable in the purchase agreement.

Why it matters: Without it, a title claim could lead to expensive legal battles or even loss of your home. Title insurance provides peace of mind for one upfront cost.

Common Costs and Who Pays What in Nevada

Closing costs typically range from 2-5% of the purchase price for buyers (and similar for sellers). Key items include:

Escrow fees (often split or negotiated)

Title insurance premiums

Recording fees

Lender fees (appraisal, origination)

Prorated taxes/HOA dues

Customs vary by county, but in Clark County, sellers often cover the owner's title policy.

Why Choose Platinum Title and Escrow?

We're not just processors—we're your local experts in Las Vegas real estate. Our team delivers clear communication, proactive problem-solving, and platinum-level service to make your closing seamless.

Ready to learn more or get a personalized estimate for your next transaction? Contact us today—we're here to answer questions and guide you every step of the way.

Your dream home deserves a flawless closing. Let's make it happen.

Comentarios